Shareholder letters: Texas Instruments, Boeing, Lockheed Martin, Adobe, Moody’s, Sherwin-Williams

TEXAS INSTRUMENTS

While I’m not an expert on semiconductor companies, I’ve been fascinated by the concentration of extraordinary leaders in the industry: Jensen Huang at Nvidia, Lisa Su at AMD and recently Pat Gelsinger at Intel are on top of my mind. I also noticed Rich Templeton from Texas Instruments while reading 2019 shareholder letters for S&P 500 companies. His letters are generally short (1-2 pages) but stuffed with no-BS language like “We will remain focused on the belief that long-term growth of free cash flow per share is the ultimate measure to generate value”. FCF per share is not a metric management generally wants investors to focus on (another famous proponent of FCF per share metric as a measure of value creation is Jeff Bezos) because it’s harder to game compared to adjusted EBITDA or earnings. Templeton also talks a lot about the importance of being passionate and company culture.

On passion and culture:

For decades, Texas Instruments has operated with a passion to create a better world by making electronics more affordable through semiconductors. With each generation, technology has become more reliable, more affordable and lower in power, with semiconductors used by a growing number of customers and markets. Our passion continues to be alive today, as we help customers develop electronics and new applications, particularly in industrial and automotive markets.

Our founders had the foresight to know that passion alone was not enough and that building a great company required a special culture to thrive for the long term. For many years, we’ve run our business with three overarching ambitions in mind. First, we will act like owners who will own the company for decades. Second, we will adapt and succeed in a world that’s ever changing. And third, we will be a company that we’re personally proud to be a part of and would want as our neighbour. When we’re successful in achieving these ambitions, our employees, customers, communities and shareholders all win.

On free cash flow per share:

As engineers, it’s a privilege to get to pursue our passion of creating a better world by making electronics more affordable through semiconductors.

We will remain focused on the belief that long-term growth of free cash flow per share is the ultimate measure to generate value. To achieve this, we will invest to strengthen our competitive advantages, be disciplined in capital allocation and stay diligent in our pursuit of efficiencies.

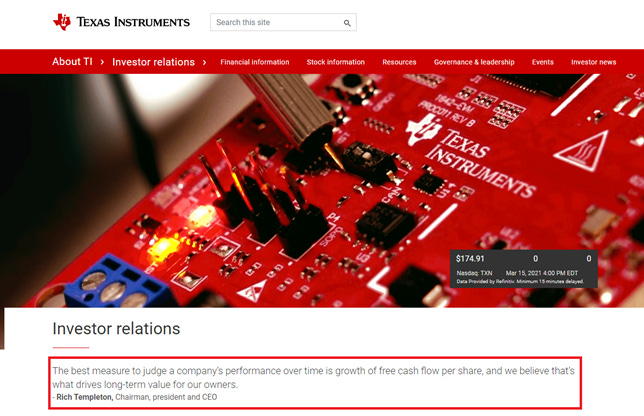

Templeton’s quote on FCF per share is literally the first thing you see when visiting their IR page:

https://investor.ti.com/static-files/47d7d7c7-f9f4-41b9-b795-13ac93428916

If you want to learn more about Rich Templeton, this is a great article:

BOEING

On return to normalcy:

Perhaps the biggest near-term uncertainty facing our industry is how quickly commercial passenger demand will rebound following the pandemic. While it is too soon to make a definitive projection, we currently anticipate that it will take approximately three years for travel to return to 2019 levels, with domestic passenger traffic improving first, followed by regional and long-haul international routes. Travel restrictions, coupled with uneven vaccine distribution across developed and developing markets, will prolong a return to normalcy. We fully expect all travel will return to a historical long-term growth trend once the pandemic is in our rearview mirror.

On limitations of video conferencing technology:

Yet we all recognize the inherent limitations of remote video conferencing technology. Spending 12 hours a day on video calls is exhausting. More importantly, it does not create space for impromptu conversations that can spark new ideas, which routinely happens when we are physically gathered in the same room. It does not produce the experience of forging new customer relationships that comes with face-to-face conversation. Let’s face it, no one ever arrives 20 minutes early for a video call. Nor does anyone linger to talk with a few colleagues after a video call abruptly ends.

On the long-term outlook for travel:

We expect demand for business and personal travel will continue to expand. Less than 20% of the world’s current population of nearly 8 billion people has ever flown on an airplane during their entire lifetime. As our global population grows to 10 billion people by 2050—and as developing nations continue to create a larger global middle class—many more people in the world will have the incentive and income to travel on a plane. At the same time, new breakthroughs in airline technology will ultimately make air travel more accessible and affordable.

LOCKHEED MARTIN

The first shareholder letter from a new CEO James Taiclet is full of dry language, mentions various new contacts awarded during the past year which makes it hard to read and impossible to get excited (although, what would you expect from a government contractor?).

Financial results:

On areas of investments and M&A:

Our commitment to innovation led to advances that will define the future of defense and deterrence in the 21st century.

We are making investments to deliver the joint all-domain operations, autonomy, hypersonics, and artificial intelligence needed by our customers in an increasingly volatile and unpredictable threat environment…

…To enhance our capabilities to take on the world’s most complex problems, we also made strategic investments to augment our portfolio of talent and technologies, including capital expenditures of $1.8 billion and $1.3 billion in independent research and development. And in November, Lockheed Martin completed its acquisition of the hypersonics portfolio of Integration Innovation Inc. (i3), a software and systems engineering company that will expand our ability to design, develop, and produce integrated hypersonic technologies.

In December, we announced we have entered into a definitive agreement to acquire Aerojet Rocketdyne Holdings, Inc., a world-recognized aerospace and defense rocket engine manufacturer. If approved by the government, the acquisition will join our complementary capabilities and enable substantial growth in areas including hypersonics, tactical missiles, integrated air and missile defense, strategic systems, and space exploration by owning a key component of our supply chain.

ADOBE

While I like Adobe and think it’s a great company, their shareholder letters are just full of clutter and meaningless phrases making them nearly impossible to read. Just think about some of these “gems”:

Our resilience is rooted in an unwavering focus on our employees, groundbreaking innovation, and our purpose, which is to harness the best of Adobe to make a significant impact in the world.

As a product company at our core, Adobe’s innovation engine continued to fire on all cylinders.

As the digital experiences company, we paved the path to leadership and innovation in a digital economy.

Adobe has always been relentlessly focused on looking around the corner, driving towards the next big market opportunity to solve customer challenges and anticipate their needs. Our bold ambitions, combined with world-class execution, have enabled our continuous growth for nearly four decades.

And my personal favourite: “People are out greatest asset”

https://www.adobe.com/content/dam/cc/en/investor-relations/pdfs/AdobeStockholderLetter2021.pdf

MOODY’S

New CEO Robert Fauber on three areas of focus:

As CEO, I am focused on three key areas to meet these market needs and realize our full potential as a global integrated risk assessment business: First, sharpening our understanding of how our customers’ needs are evolving, and delivering solutions that can draw on the breadth and depth of our capabilities. Second, investing with intent to grow and scale, deepening and extending our presence in new and expanding risk assessment markets, as we have done successfully in the Know Your Customer space. Third, collaborating, modernizing and innovating with a focus on technology interoperability and data access that allows our customers to maximize our data, analytic and technology capabilities. And of course, all of this is underpinned by supporting and developing our people so that we have the skills and culture needed to drive our business forward.

https://s21.q4cdn.com/431035000/files/doc_financials/2020/ar/Moody%E2%80%99s_Annual_Report_2020.pdf

SHERWIN-WILLIAMS

On the outlook for 2021:

By design, our Company is well-positioned to take advantage of any number of demand scenarios. Last year, we demonstrated our ability to meet the unprecedented surge in DIY architectural paint demand as several other customer segments lagged. In 2021, we see an operating environment with very solid North American new residential and residential repaint demand. The trajectory of recovery in commercial and property maintenance is likely to be choppy, and comparisons in DIY will be challenging. We anticipate industrial demand will continue to improve as the year progresses. The impact of variables such as the availability and effectiveness of COVID vaccines, the new U.S. administration and proposed stimulus and infrastructure spending are hard to gauge at this point. That said, our team is skilled at adapting to any number of conditions, and we have many opportunities to grow share in all of our businesses. We’ll continue to target growing at a rate that outpaces the market through customer-driven solutions based on innovation, value-added service and differentiated distribution.

As we did in 2020, we’ll continue making investments across the enterprise to enhance our capabilities. These investments include new stores and sales reps, capacity and productivity improvements, systems, product innovation and our digital platform. We also expect to drive continuous improvement throughout our supply chain.

https://s2.q4cdn.com/918177852/files/doc_financials/2020/ar/2020-SHW-Annual-Report.pdf